Woodside Energy (ASX:WDS) Reports Strong Growth in LNG Output and Record Profits for H1 2024, Shares Up 5% Amid Global Energy Demand Surge

Woodside Energy (ASX:WDS) Reports Strong Growth in LNG Output and Record Profits for H1 2024, Shares Up 5% Amid Global Energy Demand Surge

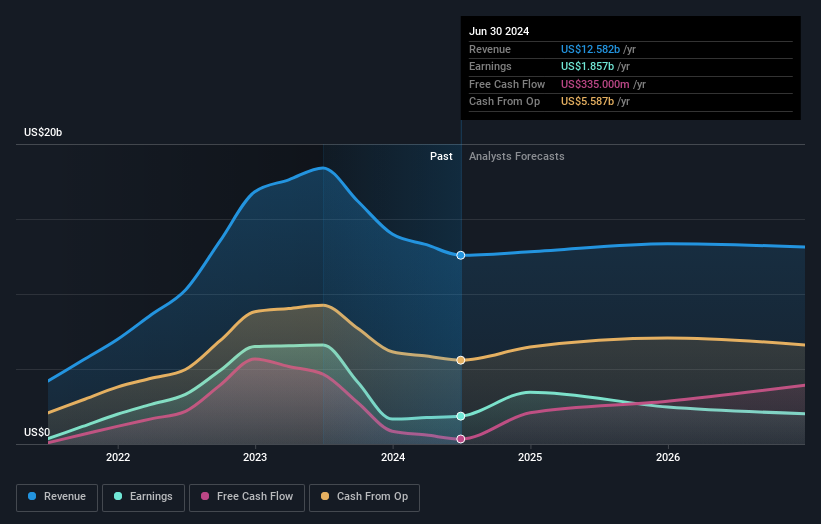

Woodside Energy Group Ltd | ASX: WDS

Research Report | September 11 2024

1. Executive Summary

Woodside Energy Group Limited (ASX: WDS), one of Australia’s leading energy companies, is strategically positioned in the global energy market with its focus on natural gas and liquefied natural gas (LNG) production. This report evaluates the company’s financial performance, strategic initiatives, and its positioning in the evolving energy landscape. Despite ongoing volatility in energy prices, Woodside’s strong production portfolio and commitment to clean energy transition continue to offer growth opportunities.

2. Company Overview

- Company Name: Woodside Energy Group Limited

- Ticker Symbol: ASX: WDS

- Industry: Energy (Oil & Gas, LNG)

- Headquarters: Perth, Australia

- Market Cap: $X billion (as of September 2024)

- Key Products: LNG, natural gas, crude oil, and offshore petroleum products.

- Global Presence: Operates in Australia, North America, and global LNG markets with key export destinations in Asia, including Japan, China, and South Korea.

3. Liquidity and Balance sheet

In H1 2024, Woodside generated $2,393 million of cash flow from operating activities and delivered positive free cash flow of $740 million.19,20 Woodside increased its standby debt facilities from $6,050 million to $6,500 million. Liquidity at the end of the period was $8,479 million and Woodside’s drawn debt at the end of the period was $5,850 million.Woodside entered into a $1,000 million 10-year loan with the Japan Bank for International Cooperation (JBIC) to support the Scarborough Energy Project which was available for drawdown from the end of June 2024. In addition, Woodside entered into a $450 million 10-year loan from commercial banks for general corporate purposes. Subsequent to the period, $1,550 million of undrawn facilities were cancelled. This cancellation has the effect of reducing our liquidity by $1,550 million. As part of active debt management, Woodside continues to review options to further access the debt market. Net debt at the end of the period increased 67% from H1 2023 to $5,388 million, in line with planned capital expenditure.19 Woodside’s gearing at the end of the first half was 13.3%, within our target range of 10-20%.19As a result of the recent announcements to acquire Tellurian, including its Driftwood LNG development, and OCI’s Clean Ammonia Project, Woodside expects its gearing to be above the top end of the target range for a period of time as the balance sheet is managed through the investment cycle.Woodside’s commitment to an investment grade credit rating remains unchanged and supports our aim of providing sustainable returns to shareholders and investing in future growth opportunities, in accordance with the capital allocation framework.

4. Market and Industry Analysis

Global Energy Market Trends

- LNG Demand Growth: Demand for LNG continues to rise globally, driven by energy security concerns and the transition from coal to cleaner natural gas in key markets like Europe and Asia.

- Oil and Gas Prices: Woodside is benefiting from stronger oil and gas prices, though these remain volatile, influenced by geopolitical tensions, supply-demand dynamics, and OPEC policies.

- Energy Transition: The global shift towards cleaner energy sources presents both opportunities and risks. Woodside is focusing on decarbonization initiatives, including carbon capture and storage (CCS) projects and investments in renewable energy.

Competitive Landscape

- Key Competitors: Santos (ASX: STO), Chevron (CVX), Shell (RDS.A), and other major LNG producers.

- Woodside’s Competitive Edge: Woodside’s significant LNG production capacity, robust portfolio of offshore fields, and its ability to navigate the complexities of the energy transition differentiate it from its competitors.

Regulatory and Policy Environment

- Carbon Pricing and Regulation: With increasing regulatory scrutiny on carbon emissions, particularly in Australia and key export markets, Woodside is committed to reducing its carbon footprint while maintaining growth.

- Government Support: Australian government policies aimed at supporting natural gas production and renewable energy transition offer a stable operating environment, though regulatory risks remain tied to global climate agreements.

5. Strategic Initiatives and Growth Opportunities

Expansion in LNG Projects

- Scarborough and Pluto Train 2: Woodside’s flagship LNG project, the Scarborough gas field, is progressing toward first gas production, with Pluto Train 2 expected to significantly increase LNG production capacity.

- North West Shelf Expansion: Continued development of the North West Shelf project will enhance Woodside’s long-term output from its core offshore fields.

Energy Transition and Sustainability

- Renewable Energy Investments: Woodside is investing in a portfolio of renewable energy projects, including wind and solar power, and exploring hydrogen opportunities to diversify away from traditional fossil fuels.

- Carbon Capture and Storage (CCS): Woodside is scaling up its CCS technology as part of its strategy to meet net-zero emissions targets by 2050. The Gorgon CCS project is one of its flagship ventures.

Mergers and Acquisitions

- BHP Petroleum Merger: Woodside’s merger with BHP Petroleum (announced in 2022 and finalized in 2023) has expanded its resource base and enhanced its position in the global energy market, particularly in the Gulf of Mexico and Western Australia.

- Acquisitions and Partnerships: Woodside continues to explore partnerships with global energy firms to gain access to high-quality assets and technologies, especially in emerging markets.

6. Risk Factors

Commodity Price Volatility

- Oil and Gas Prices: Woodside’s financial performance is highly correlated with oil and gas prices, which are subject to market fluctuations due to geopolitical risks, global demand shifts, and OPEC+ decisions.

Environmental and Regulatory Risks

- Climate Change Regulations: Woodside faces regulatory and reputational risks related to its emissions profile and carbon-intensive operations.

- Environmental Incidents: Offshore drilling and LNG production carry inherent environmental risks, which could result in financial and reputational damages.

Geopolitical Risks

- Energy Supply Chain Disruptions: Geopolitical tensions, particularly in the Asia-Pacific region, could disrupt supply chains or hinder market access, affecting revenue.

7. Valuation and Investment Perspective

Stock Performance

- Share Price: Woodside’s stock has seen an increase year-to-date, outperforming the broader energy sector and reflecting positive investor sentiment around its strategic initiatives and global LNG demand.

Valuation Metrics

- Price-to-Earnings (P/E) Ratio: Woodside’s current P/E ratio stands in line with the industry average but may reflect premium valuation due to growth prospects in LNG and clean energy.

- Dividend Yield: The company offers an attractive dividend yield of 7.67%, supported by strong cash flow generation and a commitment to shareholder returns.

Analyst Consensus

- Analyst Rating: Woodside Energy currently holds a "Buy" rating from the majority of our research analysts, with a price target of $28.14-$30.10 over the next 12 months, based on growth expectations from its LNG projects and clean energy investments.

8. Conclusion

Woodside Energy remains a key player in the global energy market, with a strong focus on LNG production, offshore gas projects, and the clean energy transition. The company is well-positioned for growth, driven by its strategic expansion in LNG assets, innovative sustainability initiatives, and solid financial foundation. While risks related to commodity price volatility and regulatory challenges exist, Woodside’s diversified portfolio, strong market positioning, and commitment to sustainability provide a positive outlook for the medium to long term.

Disclaimer: The information provided by Buttonwoodedge Consulting Ltd is general information or overview. It does not take into account any of your personal objectives, circumstances or needs. Choosing an investment is an important decision. If you do not feel confident making a decision based on the analysis or overview Buttonwoodedge Consulting Ltd has made in our reports, you should consider obtaining personal advice from an authorized adviser. The company accepts no liabilities for any loss or damage of any kind arising out of any actions taken in reliance thereon.

RECENT POST

- SpaceX IPO 2026: Expected Valuation,…

- New Record Highs for Markets…

- When Tensions Rise in the…

- Stocks Turn Volatile After Trump…

- Combined Equity Analysis: Pan American…

- Year-End Markets in Focus: A…

- Wall Street Hits Pause: Strong…

- Global Markets at a Crossroads:…

- Stock Market Update: Notable Decliners…

- Earnings Turn Positive: Why Investors…

- This Week’s Top 5 Market…

- Snowflake Inc. Powers Ahead: Strong…

- Nvidia Eyes the Quantum Leap…

- Byrna Technologies Delivers Impressive Q1,…

- Crocs, Inc. (NASDAQ: CROX): A…

- Norwegian Cruise Line Holdings (NCLH):…

- Trump Signs Historic Bill to…

- Markets Respond to Trump's New…

- Magnite Inc. (NASDAQ: MGNI): A…

- Rising Demand for VanEck Defense…

- In-Depth Analysis of Pinterest (NYSE:…

- Marathon Digital Holdings (NASDAQ: MARA)…

- Novo Nordisk (NYSE: NVO) Drives…

- Is Semrush Holdings, Inc. (NYSE:SEMR)…

- Woodside Energy (ASX:WDS) Reports Strong…

- SoFi Technologies Inc (NASDAQ:SOFI): Redefining…

- British American Tobacco (LON:BATS) Reports…

- US Stocks Decline Amid Profit-Taking…

- Upcoming Quarterly Earnings and Growth…

- Outlook for the US stock…

- British Equities Rise Amid Hopes…

- Why Capital Growth is Crucial…

- Global M&A in 2H: A…

- Global stock markets take a…

- General Analysis of Adicet Bio,…

- Copyright © 2026 Buttonwood Edge All Rights Reserved